Industry News • 28 Apr, 2026 • 5 min read

Tariff Shift April 2026: What It Means for Importers and How to Respond

By Andrea Davila

On April 6, 2026, a major shift in U.S. trade policy took effect—one that is already reshaping how importers calculate costs, assess risk, and structure their supply chains. The move from a “metal content” valuation model to a “full customs value” framework marks a fundamental change in how Section 232 tariffs are applied to imported goods.

From Metal Content to Full Value

Historically, Section 232 duties on derivative products—such as machinery and equipment—were assessed based only on the value of the steel, aluminum, or copper contained within the item. That approach left significant portions of a product’s value—like engineering, labor, and embedded technology—untouched by tariffs.

As of April 6, that’s no longer the case.

Tariffs are now applied to the total entered customs value of a product. This includes not just raw materials, but also labor, software, electronics, design, and assembly. For importers, this significantly expands the dutiable base. Depending on the product’s composition, tariffs can reach 25% or even 50% if the item contains enough covered metal to qualify.

One important nuance: if a product contains multiple covered metals (steel, aluminum, copper), the duties do not stack. Instead, the highest applicable tariff rate is applied once.

The Cost Impact Is Immediate

This shift has a direct financial impact, particularly for industries importing high-value equipment or complex machinery. Products that previously incurred relatively modest duties based on metal content are now subject to tariffs on their full value—often multiplying total duty exposure.

For companies operating on tight margins or managing large-scale imports, this change requires immediate attention and strategic adjustment.

Mitigation Strategies: Where Opportunities Exist

Despite the increased burden, there are still pathways to reduce or control tariff exposure.

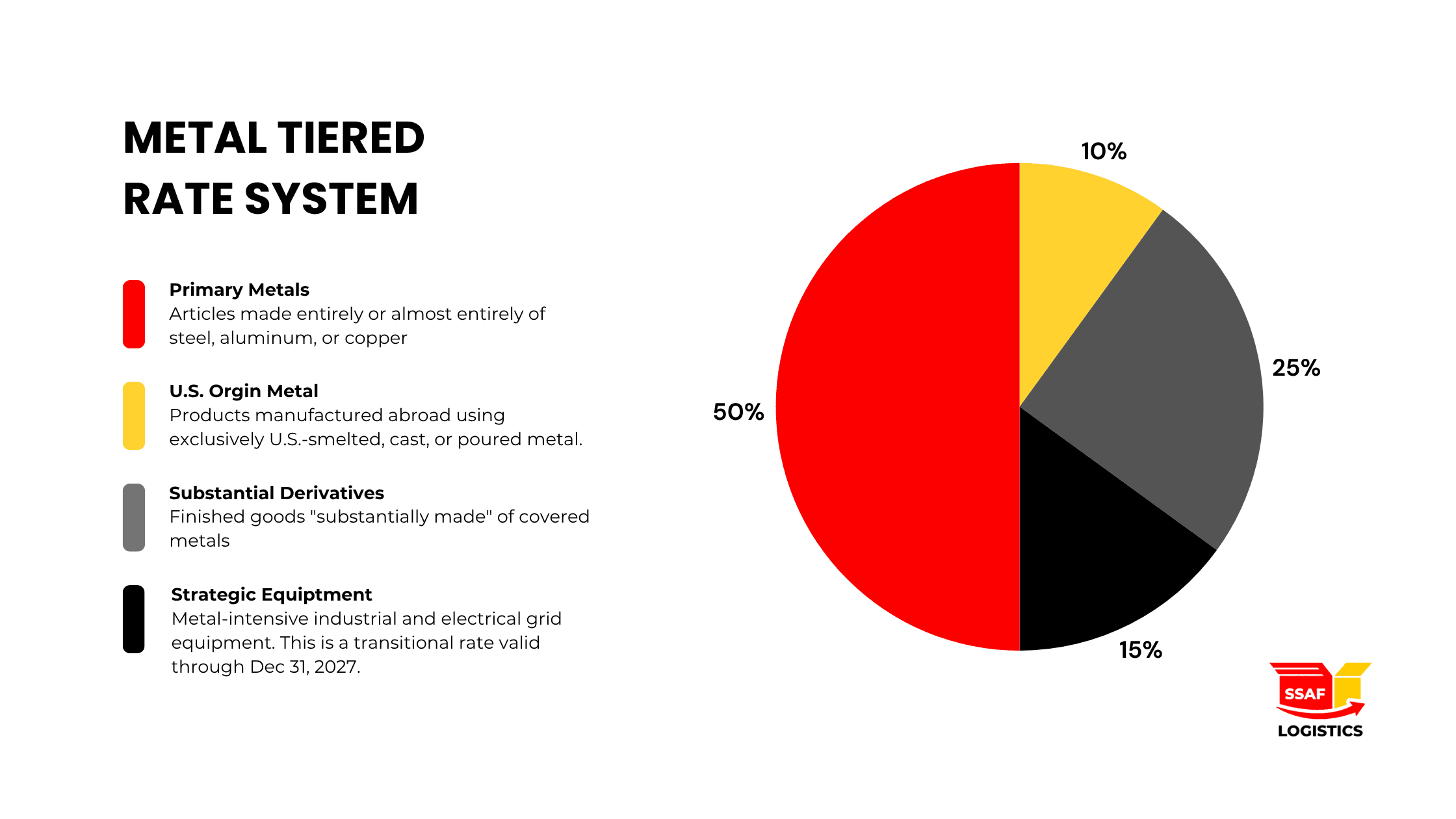

One key strategy involves leveraging the “15% Rule.” Products classified outside of HTSUS Chapters 72–76 may qualify for exemption from Section 232 tariffs if the combined metal content (steel, aluminum, copper) makes up 15% or less of the item’s total weight. This requires detailed product-level analysis and weight auditing, but when applicable, it can move goods from a tariffed category to an exempt one.

Another opportunity lies in Annex III filings. Certain goods—particularly those tied to electrical grid infrastructure and defense—can qualify for a reduced 15% transitional tariff rate. This lower rate is only guaranteed through December 31, 2027. After that, affected items revert to the standard 25% rate. Acting early allows importers to lock in savings during this limited window.

Regulatory Changes: FTZ and Drawback Implications

The policy shift also introduces tighter controls around Foreign Trade Zones (FTZs). Covered goods entering an FTZ must now be admitted under “Privileged Foreign Status.” This designation ensures that the applicable Section 232 duties are locked in at the time of entry, regardless of any transformation that occurs within the zone. In practical terms, it limits the ability to mitigate duties through FTZ-based manufacturing strategies.

At the same time, a notable opportunity has emerged.

Under the new rules, manufacturing drawback is now permitted for certain items listed in Annex I-B and Annex III. This means that if a company imports components, uses them in manufacturing, and then exports the finished product, it may be eligible to recover the Section 232 duties paid. Previously, these duties were largely non-refundable, making this a meaningful shift for exporters.

What This Means Going Forward

The April 2026 tariff changes are not just a pricing adjustment—they represent a structural shift in how import costs are calculated and managed. Companies that rely on imported machinery, components, or metal-intensive goods will need to reassess classifications, review sourcing strategies, and explore eligibility for exemptions or recovery programs.

Those that act quickly—by auditing product compositions, filing for transitional rates, and aligning with the new regulatory framework—will be better positioned to control costs and maintain operational efficiency in a more complex trade environment.

Related Blog Posts

![[object Object]](/_next/image?url=https%3A%2F%2Fcdn.sanity.io%2Fimages%2Fj6rggeis%2Fproduction%2F7ad625a0410e359fd61ef0773f77e1800b510c03-2240x1260.png&w=3840&q=75)

![[object Object]](/_next/image?url=https%3A%2F%2Fcdn.sanity.io%2Fimages%2Fj6rggeis%2Fproduction%2F2f1f139cc766e1ade60d1668908d10f6406721ff-2240x1260.png&w=3840&q=75)

![[object Object]](/_next/image?url=https%3A%2F%2Fcdn.sanity.io%2Fimages%2Fj6rggeis%2Fproduction%2F4d41da7b56424c35af0d33fe2194588ac02959a3-2240x1260.png&w=3840&q=75)

![[object Object]](/_next/image?url=https%3A%2F%2Fcdn.sanity.io%2Fimages%2Fj6rggeis%2Fproduction%2Ffcab86688e70f3357cd15916f07e8bf8f896f1dd-2240x1260.png&w=3840&q=75)